As we discussed in “How Businesses Accept Credit Card Payments Online: A Complete Guide for Global Merchants,” most customers never think about what happens after they click “Pay Now.”

For businesses, though, that moment is everything.

Whether you run an online store, a digital platform, or a global service business, your ability to accept credit card payments depends on one core setup: a credit card merchant account. Without it, payments stop. Revenue stops. Growth stops.

This article explains what a merchant account really is, how it works behind the scenes, and why it matters even more for high-risk and international businesses in 2026.

What Is a Credit Card Merchant Account?

A credit card merchant account is a financial account that allows your business to accept credit card payments from customers. It doesn’t replace your regular bank account. Instead, it acts as a temporary holding space for card payments before the funds are transferred to you.

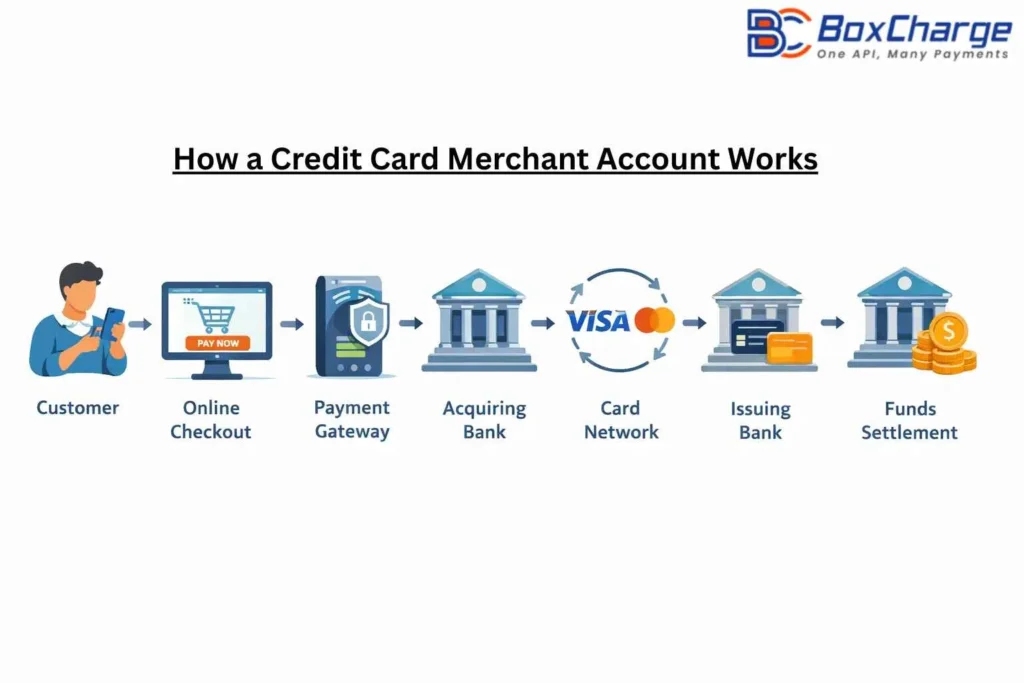

When a customer pays online, the money doesn’t move directly into your bank account. It goes through a short but critical journey. The merchant account sits right in the middle of that process, making sure funds are authorized, cleared, and settled properly.

If your business wants to accept payment online, a merchant account is non-negotiable.

How a Merchant Account Actually Works

Here’s what happens when a customer enters their card details on your website:

First, the payment information is securely sent through a payment gateway. The gateway passes the data to the acquiring bank connected to your merchant account. That bank then checks with the customer’s card network and issuing bank to confirm the transaction.

If the payment is approved, the funds are authorized and placed in your merchant account. After a short settlement period—usually a few days—the money is transferred to your main business account.

From the customer’s side, this takes seconds. On the backend, multiple systems are working together to manage risk, fraud, and compliance.

Merchant Account vs Payment Gateway (Why Both Matter)

Many business owners confuse merchant accounts with payment gateways. They serve different purposes.

A payment gateway handles the secure transmission of card data.

A merchant account handles the money.

You need both to accept credit card payments smoothly. Most modern providers bundle them into a single credit card payment solution, which is easier to manage and safer for growing businesses.

Why Some Businesses Are Considered High Risk

Not all businesses are treated the same by banks and processors. Businesses operating in regulated or high-risk sectors face a different payment reality

Industries with higher refund rates, chargebacks, or regulatory pressure are usually classified under high-risk merchant accounts. This doesn’t mean the business is doing anything wrong. It simply means the payment risk is higher.

Examples include:

- Forex platforms and forex payment processing

- Casino and gaming platforms

- Adult content businesses

- Subscription-based dating platforms

- Online dating merchant accounts

- Cross-border digital services

These businesses often struggle to get approved through traditional banks, which is why specialized high-risk payment gateways exist.

How High-Risk Merchant Accounts Work

High-risk payment processing comes with additional controls.

Providers may require:

- Stronger fraud prevention tools

- Clear refund and dispute policies

- Ongoing transaction monitoring

- Reserves to cover potential chargebacks

While this adds complexity, it also creates stability. In 2026, card networks and regulators expect more transparency and tighter controls—especially for international payment gateway setups.

For high-risk businesses, working with the right provider is more important than finding the cheapest rate.

The Role of International Payment Gateways

If your customers come from different countries, you need more than a domestic setup.

An international payment gateway allows you to process payments across borders, handle multiple currencies, and work with local acquiring banks. This often leads to better approval rates and fewer payment failures.

For businesses involved in global payment processing, this setup is no longer optional. It’s part of operating responsibly and at scale.

Why Alternative Payment Methods Matter

Credit cards are still widely used, but they’re not the only option anymore.

Alternative Payment Methods—such as wallets, local bank transfers, and region-specific payment options—play a growing role in reducing risk and improving conversions.

For high-risk businesses, APMs can lower dependency on card networks and help manage chargeback exposure more effectively.

A strong online merchant account strategy in 2026 usually combines cards with alternative payment methods.

Credit Card Merchant Accounts for High-Risk and International Businesses

For businesses operating in regulated or high-risk industries, setting up a credit card merchant account is rarely straightforward. Sectors like forex, gaming, adult content, and online dating often require specialized high-risk merchant accounts that work with international payment gateways and support global payment processing.

These setups are designed to handle higher transaction volumes, cross-border payments, and stricter compliance requirements while still allowing businesses to accept credit card payments reliably.

Choosing the Right Merchant Account Provider

The biggest mistake businesses make is choosing a provider that doesn’t understand their industry.

High-risk business processing requires experience, flexibility, and realistic expectations. A good provider looks beyond just approvals. They help structure your payment flow in a way that lasts.

This is where platforms like Boxcharge focus—supporting high-risk, international, and fast-growing businesses with payment setups built for real-world challenges.

Final Thoughts

A credit card merchant account is not just a technical requirement. It’s the foundation of your revenue system.

If your business plans to accept credit card payments, operate globally, or scale in a high-risk sector, understanding how merchant accounts work will save you time, money, and frustration.

Payments are no longer just about getting approved. They’re about staying approved.

And choosing the right structure early can make all the difference as your business grows.

If your business operates in a high-risk or international environment, exploring a payment setup designed for long-term stability—not shortcuts—can help prevent issues before they start.

Frequently Asked Questions

What is the difference between a merchant account and a payment gateway?

A merchant account holds and settles card payments, while a payment gateway securely transfers payment data between the customer, bank, and card network. Most businesses need to accept credit card payments online.

Can high-risk businesses get a credit card merchant account?

Yes. High-risk businesses such as forex platforms, gaming sites, adult content businesses, and online dating platforms can get approved through specialized high-risk merchant accounts designed to manage higher dispute and fraud exposure.

How long does it take to receive funds from a merchant account?

Most merchant accounts settle funds within two to five business days. Settlement time can vary based on the business type, risk level, and the acquiring bank involved.