Getting a high-risk merchant account approved in 2026 is no longer the hard part.

Keeping it live is.

Across industries like Forex, online gaming, adult platforms, dating websites, and subscription businesses, merchant accounts are being approved faster than ever — and shut down just as quickly. Funds get frozen. Reserves appear overnight. Processing limits shrink without warning.

Not because the business is illegal.

Not because rules were broken.

But because risk behavior changed after approval.

This guide explains how high-risk merchant accounts actually work in 2026, what banks and payment processors monitor first, and how BoxCharge helps high-risk businesses build payment infrastructure that survives growth — not just onboarding.

What Is a High-Risk Merchant Account in 2026?

A high-risk merchant account is a payment processing setup designed for businesses operating in industries that banks consider sensitive due to dispute exposure, regulatory complexity, or cross-border transaction activity.

These include:

- Forex brokers and trading platforms

- Online casinos and gaming websites

- Adult content and subscription platforms

- Online dating websites and apps

- High-volume SaaS or subscription businesses

Unlike standard merchant accounts, high-risk merchant accounts are monitored continuously, not just at approval.

In 2026, approval means:

“We’re willing to observe your transaction behavior.”

It does not mean:

“This account is safe long-term.”

That distinction matters.

Why High-Risk Merchant Accounts Fail After Approval in 2026?

Most merchants assume accounts fail due to chargebacks or fraud.

In reality, most failures are behavioral, not intentional.

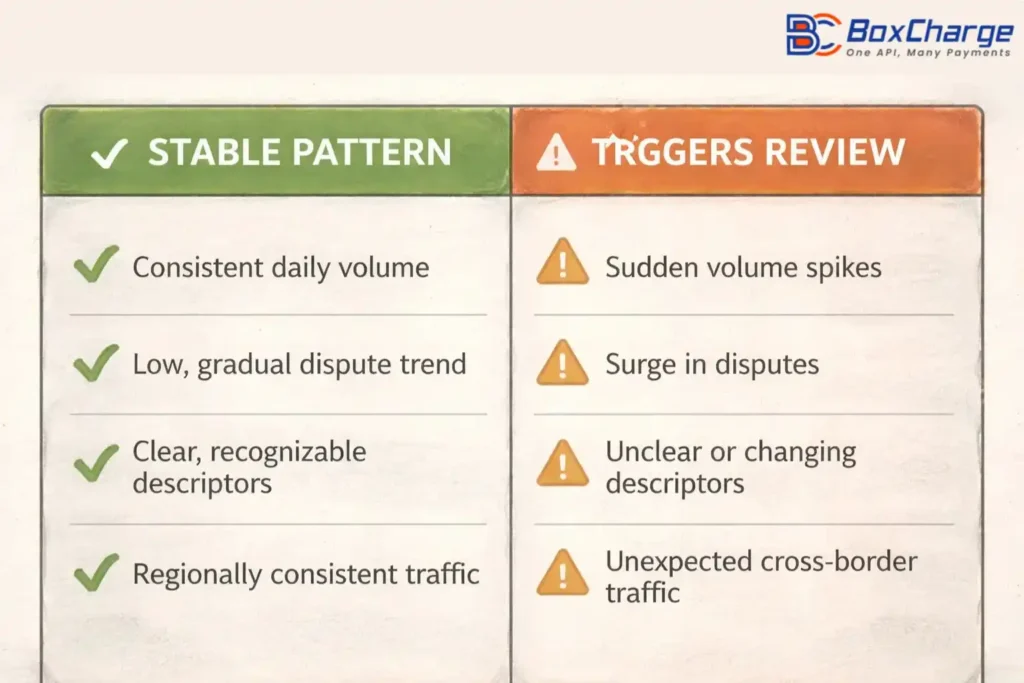

Banks and card networks now evaluate:

- How volume grows

- How disputes appear over time

- How customers recognize charges

- How payments move across regions

Approval is based on projections.

Reviews are based on actual data.

This is why many high-risk businesses experience freezes within the first 30–90 days.

The Biggest Misunderstanding: Chargeback Ratios Aren’t the First Trigger

Chargeback ratios still matter — but they are rarely the first signal.

What banks monitor earlier:

1. Dispute Velocity

Not how many disputes you have — how fast they arrive.

Ten disputes spread over a month is very different from ten disputes in 48 hours.

Clusters trigger reviews faster than ratios.

This is especially common in:

- Adult merchant accounts

- Online dating merchant accounts

- Subscription-based platforms

2. Volume Growth Patterns

Banks expect growth — but structured growth.

Risk increases when they see:

- Sudden 200–500% spikes

- Campaign-driven volume surges

- Inconsistent ticket sizes

High-risk payment processing must scale intentionally, not explosively.

3. Billing Descriptor Confusion

“Unrecognized Charge” disputes remain one of the biggest silent killers.

This happens when:

- The descriptor doesn’t match the website name

- The brand operates multiple domains

- The customer forgets the context of the purchase

Banks interpret this as merchant clarity risk, not customer error.

4. Cross-Border Transaction Behavior

Global businesses are expected to operate internationally.

What triggers scrutiny:

- Traffic from undeclared regions

- Sudden shifts in country mix

- Cross-border retries from the same cards

This affects:

- Forex payment processing

- Online gaming payment solutions

- International dating platforms

High-Risk Merchant Account Licensing: What Helps and What Doesn’t

Licensing matters — but not the way most merchants think.

Easier-Entry Jurisdictions

Examples: Curacao, Anjouan, and certain offshore jurisdictions.

Pros

- Faster go-live

- Lower upfront cost

- Broad acceptance for international payments

Cons

- Higher monitoring intensity

- More reliance on clean transaction behavior

- Often paired with rolling reserves

Tier-1 Regulatory Jurisdictions

Examples: UK, Malta, EU-regulated environments.

Pros

- Higher bank confidence

- Lower long-term scrutiny

- Easier access to stable acquiring

Cons

- Long approval timelines

- Strict reporting obligations

- Less flexibility for experimentation

Important note:

No license guarantees stability.

Banks evaluate licensing alongside transaction behavior, not instead of it.

Why Generic Payment Processors Fail High-Risk Businesses

Most low-risk processors aren’t bad — they’re just mismatched.

They struggle because:

- Fraud rules are static

- Risk tolerance is low

- Cross-border routing is limited

- Underwriting and monitoring teams are disconnected

This is why many high-risk merchants outgrow their first processor quickly.

High-risk payment gateways must adapt as risk evolves.

How BoxChargeApproaches High-Risk Merchant Accounts Differently

BoxCharge doesn’t sell “instant approval” or “no-limit processing.”

That language doesn’t survive contact with banks.

Instead, BoxCharge focuses on predictability — the one thing banks care about most.

1. Behavior-Aligned Account Structuring

Before volume flows, BoxCharge evaluates:

- Expected ticket sizes

- Growth curves

- Geography exposure

- Payment method mix

The goal is alignment with underwriting expectations.

2. Dispute Velocity Management (Not Just Ratios)

Two merchants can have the same chargeback ratio.

Only one gets shut down.

BoxCharge helps structure:

- Refund timing

- Retry logic

- Descriptor clarity

- Dispute distribution

This reduces clustering — a key early-warning trigger.

3. Modular High-Risk Payment Infrastructure

High-risk businesses don’t need one rigid solution.

They need components:

- Single or multi-MID merchant accounts

- International acquiring

- Alternative payment methods for volume balancing

- Optional crypto settlement where appropriate

This flexibility signals operational maturity.

4. Cross-Border Payment Readiness

For businesses accepting payments globally, BoxCharge designs:

- Region-aware routing

- Issuer-friendly flows

- Market-specific risk tolerance

This supports global payment processing without triggering constant reviews.

Industries BoxCharge Supports

BoxCharge works with regulated and high-risk industries that require long-term payment stability, including:

- High-risk merchant accounts

- Forex merchant accounts

- Online gaming and casino merchant accounts

- Adult merchant accounts

- Online dating merchant accounts

- Subscription-based digital platforms

The focus is always the same: stability over speed.

When a High-Risk Merchant Account Strategy Makes Sense

This approach is ideal for businesses that:

- Plan to scale internationally

- Prioritize settlement continuity

- Accept risk as manageable, not avoidable

It is not ideal for:

- Short-term experiments

- Arbitrage-driven models

- Businesses chasing fast approval without structure

Being selective builds trust — with banks and with serious merchants.

Final Thought: Approval Is Easy. Stability Is Engineered.

In 2026, high-risk merchant accounts don’t fail because businesses are bad.

They fail because payment foundations weren’t built to survive success.

Banks don’t expect perfection.

They expect predictability.

And predictability is something you design — not something you hope for.

Request a High-Risk Payment Readiness Review

If you’re planning to launch or scale a high-risk business and want to understand whether your payment setup can survive real growth, BoxCharge starts with an honest assessment.

In a short review, we identify how your transaction behavior may be interpreted by banks — before issues surface.

That’s how sustainable processing begins.