Accepting credit card payments online looks simple from the outside. Add a checkout page, connect a payment provider, and start selling.

That’s how it works in theory.

In reality, businesses discover very quickly that payments are not just a technical setup. They’re a risk system. And for many industries, especially global and high-risk ones, payments become the most fragile part of the business.

This is where most merchants get stuck — not because demand is missing, but because the payment foundation isn’t built for growth.

What “Accept Credit Card Payments Online” Really Means

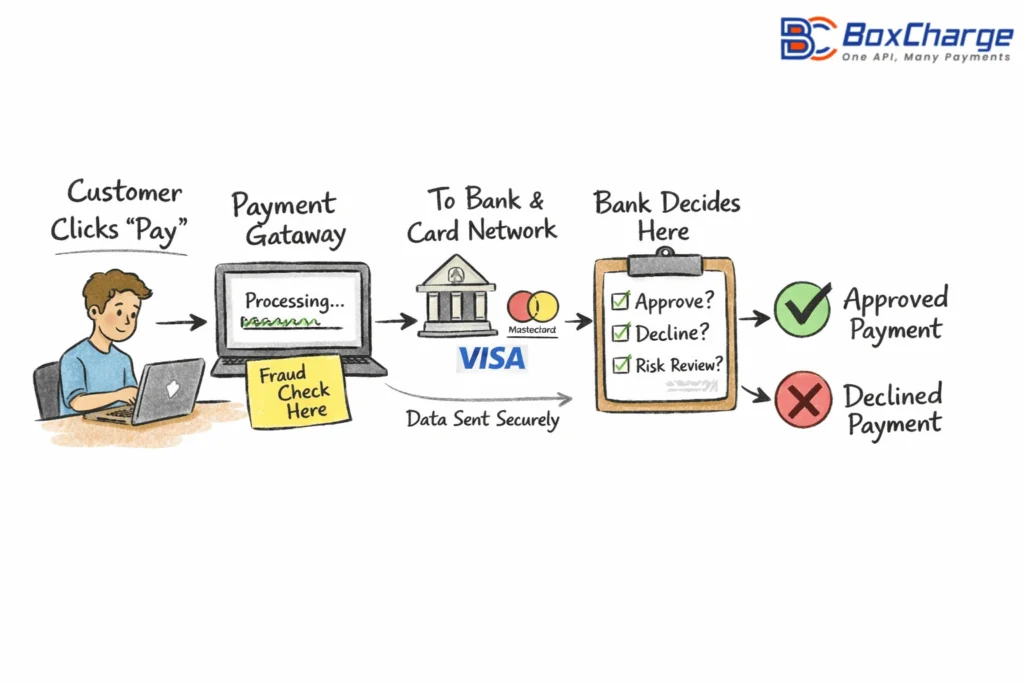

When customers enter their card details, a lot happens behind the scenes in a few seconds.

A proper credit card payment solution usually includes:

- A credit card merchant account

- A payment gateway

- An acquiring bank

- Card networks like Visa and Mastercard

- Fraud and compliance checks

If any one of these layers breaks, payments stop.

This is why simply “accepting payment online” is not the same as building a stable payment system.

The Merchant Account Is the Real Gatekeeper

For most businesses, a stable online merchant account setup determines whether credit card payments run smoothly or collapse once volume starts increasing.

A credit card merchant account is where the real approval happens.

Banks don’t just look at your website. They assess:

- Your business model

- Your refund behavior

- Customer complaints

- Geographic exposure

- Industry risk

For low-risk stores, approvals are quick.

For others, it’s a different story.

Why High-Risk Merchant Accounts Exist

Certain industries face more disputes, regulations, or fraud exposure by default. That doesn’t make them illegal. It just makes banks nervous.

This is where high-risk merchant accounts come in.

Industries commonly classified as high-risk include:

- Forex merchant accounts and trading platforms

- Gaming and casino merchant accounts

- Adult merchant accounts

- Online dating merchant accounts

- Subscription-based digital services

These businesses often struggle with:

- Sudden account freezes

- High rolling reserves

- Delayed settlements

- Payment gateway shutdowns

Many merchants only realize they’re “high-risk” after their account gets restricted.

Credit Card Payments and Global Expansion Don’t Mix Easily

Selling internationally adds another layer of complexity.

With global payment processing, merchants face:

- Currency conversion issues

- Regional compliance rules

- Cross-border fraud monitoring

- Higher dispute ratios

An international payment gateway is not optional here — it’s essential.

Without it, businesses often experience:

- Higher decline rates

- Card network scrutiny

- Country-level blocks

This is why global merchants rarely survive with a single acquiring bank.

Why High-Risk Payment Processing Fails So Often

Most failures don’t come from fraud.

They come from misalignment.

Banks expect predictability.

High-risk businesses rarely behave predictably.

Examples:

- Forex users dispute trades after losses

- Dating users forget subscriptions

- Adult customers request discreet refunds

- Gaming users misunderstand bonus terms

None of this is unusual — but card networks treat patterns, not intentions.

This is where high-risk payment processing requires a different setup.

Credit Card Merchant Accounts for High-Risk and International Businesses

For businesses operating in regulated or high-risk industries, merchant accounts come with additional requirements. Forex, gaming, adult, and dating platforms often need specialized high-risk merchant accounts that support international payment gateway setups and global payment processing.

These accounts are structured differently, often involving higher scrutiny, layered compliance checks, and region-specific acquiring relationships. Without this structure, payment stability becomes fragile as volume grows.

The Role of Alternative Payment Methods

Relying only on cards increases pressure.

That’s why many businesses now use Alternative Payment Methods alongside credit cards:

- Local bank transfers

- Digital wallets

- Region-specific options

This doesn’t replace cards — it protects them.

By spreading transaction volume, merchants reduce:

- Chargeback concentration

- Visa monitoring exposure

- Sudden account shutdowns

For high-risk businesses, this balance is critical.

Industry-Specific Payment Realities

1: Forex & Trading Platforms: Forex payment processing deals with emotional disputes. Even legitimate trades get challenged. Without dispute buffers, accounts don’t last long.

2: Gaming & Casino Businesses: Gaming merchant accounts must carefully manage recurring billing, bonuses, and regional restrictions. One spike in disputes can trigger monitoring programs.

3: Adult Industry: Adult merchant accounts face privacy-driven chargebacks. Billing descriptors and refund policies matter more than marketing.

4: Online Dating Platforms: Online dating merchant accounts often fail because cancellations and expectations are unclear. Payments suffer even when the platform performs well.

Each industry requires a tailored high-risk Business Processing approach.

Why Payment Stability Matters More Than Approval

Many providers promise “instant approval.”

That’s not the real problem.

The real question is:

Will payments still work after 6 months?

Stable systems focus on:

- Multiple acquiring banks

- Early dispute tracking

- Geographic traffic control

- Risk-aware checkout design

This is where short-term approvals fail, and long-term strategies win.

Where BoxCharge Fits In

BoxCharge works with businesses that don’t fit into standard banking boxes.

The focus isn’t on quick wins.

It’s building payment setups that survive:

- Chargeback cycles

- Volume spikes

- International expansion

By combining high-risk payment gateway services, global acquiring relationships, and alternative payment methods, merchants gain flexibility instead of constant risk.

Final Thoughts

Accepting credit card payments online is no longer just about technology. It’s about risk tolerance, structure, and foresight.

In 2026, businesses that treat payments as an afterthought struggle to scale. Those who build payment infrastructure early operate with fewer interruptions and more control.

If your business operates in a high-risk or global space, payment stability isn’t optional — it’s survival. A well-structured online merchant account, paired with the right gateway and processing strategy, makes growth possible without constant fear of shutdowns.