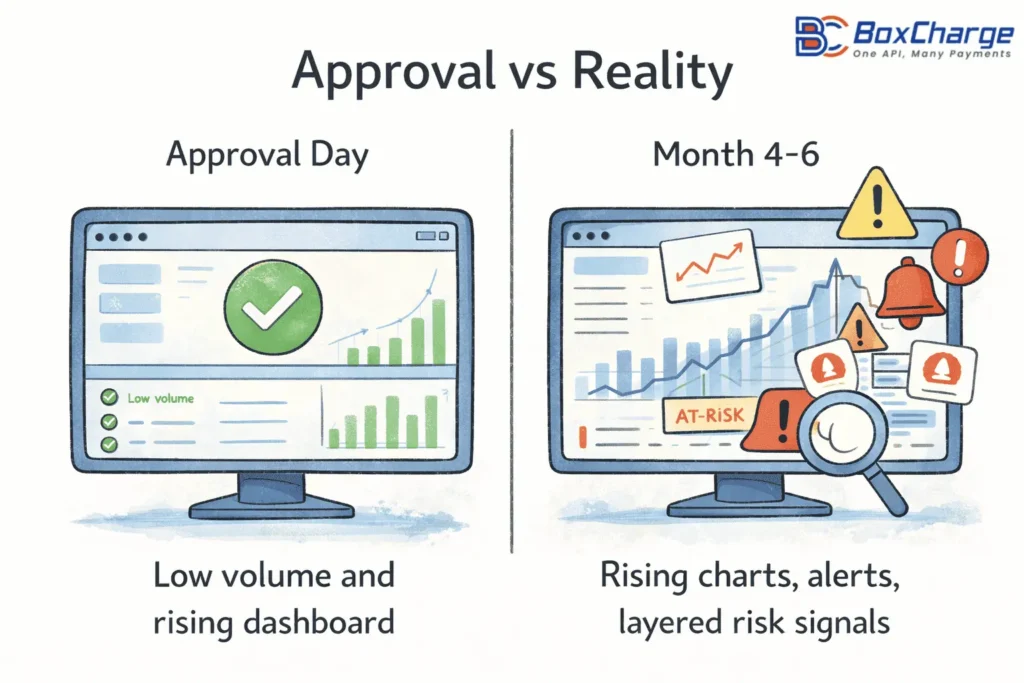

Getting approved for a high-risk merchant account often feels like crossing the finish line.

In reality, it’s just the starting point.

For many businesses operating in regulated or complex environments, approval is followed by a far more fragile phase — one where transaction patterns evolve, volumes increase, and acquiring banks begin reassessing risk in real time.

As we explain in our guide to international high-risk payment processing, this is the stage where most payment setups quietly break, not because of fraud, but because the infrastructure was never built to handle growth.

We’ve seen it happen repeatedly. Accounts don’t fail overnight. They slowly destabilize until payments stop working altogether.

This article explains why.

Built for Stability, Not Hype

High-risk businesses don’t need promises of instant approval or unlimited processing.

They need a payment infrastructure that stays live when volume grows.

The businesses that survive are usually the ones that prioritize predictable processing behavior over speed. They understand that banks value consistency, clarity, and control — not aggressive scaling without structure.

If payments are critical to your operation, interruptions aren’t an inconvenience. They’re a threat to the business itself.

Who This Applies To (And Why)

“High-risk” isn’t just about what you sell.

It’s about how your business operates

This problem most often affects merchants with:

- Recurring billing or subscription models

- Cross-border card volumes

- Expansion into multiple jurisdictions

- Regulated or compliance-heavy operations

- Business models where customer lifetime value matters more than one-time sales

This pattern is especially common in regulated business models like forex and gaming, where transaction behavior evolves faster than bank risk tolerance.

The Real Reason Accounts Fail After Approval

Here’s the part most processors don’t explain clearly:

Approvals don’t fail. Risk models change.

Banks don’t make a one-time judgment. They continuously evaluate patterns as volume, geography, and customer behavior shift. What looked acceptable at $30,000 per month may trigger concern at $300,000 — even if nothing “wrong” happened.

Some realities we see often:

- Growth itself triggers automated reviews

- Chargebacks are only one of many risk signals

- Refund timing, dispute velocity, and region mix matter

- Sudden volume spikes attract scrutiny regardless of intent

Banks respond to patterns, not explanations.

Good intentions don’t prevent reviews — structure does.

How We Approach the Problem at BoxCharge

We don’t focus on shortcuts.

We focus on predictability.

At BoxCharge payment infrastructure, our focus is not on shortcuts, but on designing transaction behavior that banks can consistently underwrite. That means thinking beyond approval and designing payment flows that remain stable under ongoing scrutiny.

In practice, this includes:

- Structuring volume increases intentionally, not reactively

- Managing dispute velocity, not just headline ratios

- Aligning transaction flow with acquiring bank expectations

- Designing setups that hold up during long-term monitoring

The goal isn’t to look “safe” for a month.

It’s to remain viable a year later.

This is where a purpose-built high-risk payment gateway becomes less about approval speed and more about long-term predictability under bank monitoring.

Payment Infrastructure Is Modular — Not One Account

Most failures occur when a high-risk merchant account structure is treated as a single product instead of a system designed to absorb growth.

Sustainable setups are built from components.

Depending on the business model, this may include:

- One or multiple merchant accounts (MIDs)

- International acquiring to balance regional exposure

- Smart routing based on geography and transaction behavior

- Alternative rails to reduce card network pressure

- Stablecoin settlement (such as USDC or USDT) or instant bank transfers via Open Banking, where jurisdictionally appropriate

These alternatives aren’t replacements for cards. They act as pressure valves, allowing merchants to distribute volume intelligently when card scrutiny increases.

Flexibility is not about complexity.

It’s about control.

Why Generic Processors Struggle With High-Risk Models

Most low-risk processors aren’t doing anything wrong. They’re simply not designed for this level of nuance.

Common limitations include:

- Static fraud rules that don’t adapt as behavior evolves

- Domestic processing rails forced onto global businesses

- Underwriting teams that change between review cycles

- Risk tolerance calibrated for low-variance merchants

High-risk businesses don’t need volume permission.

They need underwriting continuity.

Without it, instability builds quietly until the account fails.

Risk, Compliance, and Long-Term Survivability

There’s a misconception that successful processing means eliminating risk.

In reality:

The goal isn’t to eliminate risk.

It’s to make risk predictable.

That involves:

- Awareness of card network monitoring programs

- Transparent handling of disputes and refunds

- Regulatory adaptability across regions

- Planning for survivability, not perfection

Zero-risk promises don’t build trust.

Controlled exposure does.

Frequently Asked Questions

1: Should I expect reserves on a high-risk merchant account?

Yes. Most high-risk merchant accounts in 2026 include rolling reserves as a standard risk-balancing mechanism. What matters is how the reserve is structured and whether it adjusts as risk stabilizes.

2: How long does approval usually take?

Approval timelines typically range from several business days to a few weeks. Timing depends on structure, documentation, jurisdiction, and processing history — not speed claims.

3: Can high-risk merchants process international payments reliably?

Yes, with the right acquisition strategy. International processing works best when transaction behavior is aligned with regional banking expectations rather than routed through a single domestic setup.

4: What happens if my transaction volume spikes suddenly?

Unplanned spikes usually trigger reviews. Structured growth that’s planned, communicated, and supported by routing logic is far more sustainable.

5: What options exist if card network pressure increases?

Merchants typically rebalance volume. This may involve bank transfers through Open Banking or stablecoin settlement (such as USDC or USDT), depending on jurisdiction and compliance requirements.

When This Approach Makes Sense — And When It Doesn’t

This structure works best for businesses that:

- Plan to scale deliberately

- Value stability over speed

- Understand payments as infrastructure, not a feature

It may not be suitable for:

- Short-term or experimental projects

- Businesses chasing quick approvals

- Merchants are unwilling to adapt operational behavior

Being selective isn’t exclusionary.

It’s protective.

A Calm Next Step

If you’re questioning whether your current setup can survive growth, the right starting point isn’t another application.

It’s an honest assessment.

At BoxCharge, we can review your payment structure and discuss whether it’s designed to scale — before anything else.

No pressure.

No guarantees.

Just clarity.