Navigating the Labyrinth of International High-Risk Payment Processing in 2026

Why International High-Risk Payment Processing Is Harder Than Ever as We Approach 2026? For most standard e-commerce businesses, payments are a utility — a simple layer that enables them to accept payment online and move on. For high-risk merchants operating internationally, payments function very differently. They are a strategic pressure point that can determine whether a business scales sustainably or faces sudden disruption.

Banks and card networks use the term high risk to describe businesses with elevated chargeback exposure, higher average transaction values, regulatory complexity, or operations in tightly monitored or evolving legal environments. This includes sectors such as online gaming, forex, adult services, and casino platforms. When these business models expand across borders, the complexity of managing a high-risk payment solution does not increase gradually — it compounds.

As the industry moves toward 2026, the challenge has shifted well beyond simply securing a credit card merchant account. High-risk businesses must now navigate aggressive bank de-risking, automated card-network enforcement, AI-driven fraud, and fragmented global compliance frameworks — all while maintaining the ability to accept credit card payments reliably.

The Perennial Threat: Institutional De-Risking

The most serious threat facing businesses that rely on high-risk merchant accounts remains the sudden loss of payment processing capabilities. This risk stems from institutional de-risking — a strategy where banks and Tier-1 acquirers exit entire industries rather than invest in the infrastructure required to monitor them.

Industries such as online gaming, CBD, supplements, adult platforms, and casino operations are frequently impacted. Even merchants with strong processing histories can lose access when upstream correspondent banks reassess their risk appetite.

In international setups, this risk is amplified. A gaming merchant account may function smoothly under a European acquirer, only to be disrupted when the correspondent bank responsible for USD settlements withdraws support. The result is often an immediate halt in global payment processing.

For this reason, redundancy has become a baseline requirement. By 2026, experienced merchants operating in high-risk sectors typically maintain multiple online merchant accounts across jurisdictions such as Cyprus, Curacao, or Mauritius. This structure allows transaction volume to be rerouted when one region becomes unavailable, preserving continuity in high-risk payment processing.

The Billing Descriptor and the 22-Character Trap

One of the most underestimated contributors to chargebacks is the billing descriptor — the brief line of text a customer sees on their bank statement when they accept credit card payments. Most card networks limit this field to approximately 20–22 characters.

In high-risk industries, friendly fraud accounts for a significant portion of disputes. Customers often do not recognize a transaction when the descriptor reflects a holding company rather than the consumer-facing brand. This is particularly common for casino merchant accounts, adult merchant accounts, and gaming platforms operating multiple brands.

International issuing banks may further truncate descriptors or replace them with generic references, eliminating the only recognition point a cardholder has. To address this, many merchants are adopting dynamic descriptors that reflect the transaction source or domain. While this improves clarity, descriptor optimization remains constrained by legacy issuing systems and continues to influence chargeback ratios in global high-risk payment gateways.

The Financial Strain of Reserves and Settlement Delays

High-risk payment fees are visible. The pressure created by cash-flow constraints is less obvious — and often more damaging.

Processors typically impose rolling reserves, holding between 5% and 10% of monthly processing volume for periods that can extend to 180 days. For a business processing $1 million per month, this can result in hundreds of thousands of dollars being inaccessible at any given time.

Settlement delays further widen the gap between revenue generation and liquidity. International merchants using a credit card payment solution may wait 7 to 14 days to receive funds, limiting their ability to reinvest in marketing, inventory, or platform growth.

As the industry approaches 2026, some businesses are exploring stablecoin-based settlements to reduce dependence on traditional banking timelines. While these models can accelerate access to funds, they introduce additional challenges around compliance, accounting, and reliable on- and off-ramps into the fiat ecosystem.

Automated Enforcement and the Shrinking Margin for Error

Card-network oversight has shifted from discretionary review to automated enforcement. Visa’s Acceptance Monitoring Program (VAMP), expected to be fully standardized as the industry moves into 2026, applies penalties based on predefined thresholds rather than contextual analysis.

In previous years, merchants could address temporary increases in chargebacks through remediation plans. Today, exceeding monitoring thresholds can trigger automatic fines, higher processing costs, or termination of a high-risk payment gateway relationship.

For international merchants, localized fraud events are especially dangerous. A short-term attack from one region can affect global ratios, impacting approval rates across an international payment gateway and pushing merchants closer to MATCH listing.

AI-Driven Fraud and the Escalating Arms Race

As we move toward 2026, artificial intelligence is reshaping both fraud and fraud prevention. Fraud networks now use generative tools to create synthetic identities, automate dispute filings, and generate narratives that challenge traditional defenses.

High-risk merchants — including those operating forex merchant accounts and forex payment processing models — are frequent targets due to their existing scrutiny. Issuing banks increasingly favor cardholders, requiring merchants to submit comprehensive evidence to win disputes.

In response, many businesses are investing in layered fraud orchestration systems that combine device fingerprinting, behavioral analysis, velocity controls, and real-time risk scoring. While effective, these systems add cost per transaction and further tighten margins for high-risk payment processing.

The Compliance Patchwork

Cross-border operations require compliance with overlapping regulatory regimes. In Europe, PSD3 has expanded Strong Customer Authentication requirements. While this reduces fraud, it can negatively impact conversion rates for high-emotion or impulse purchases.

Merchants offering global payment processing must also manage data protection laws, tax obligations, and regional payment rules. Expansion into India, for example, introduces RBI data localization requirements that mandate domestic storage of payment data.

Managing these parallel compliance environments requires technical infrastructure and legal oversight — resources that many mid-sized merchants struggle to maintain internally.

The Path Forward: Strategy Over Technology

Surviving the international high-risk payments landscape approaching 2026 requires strategy, not isolated tools.

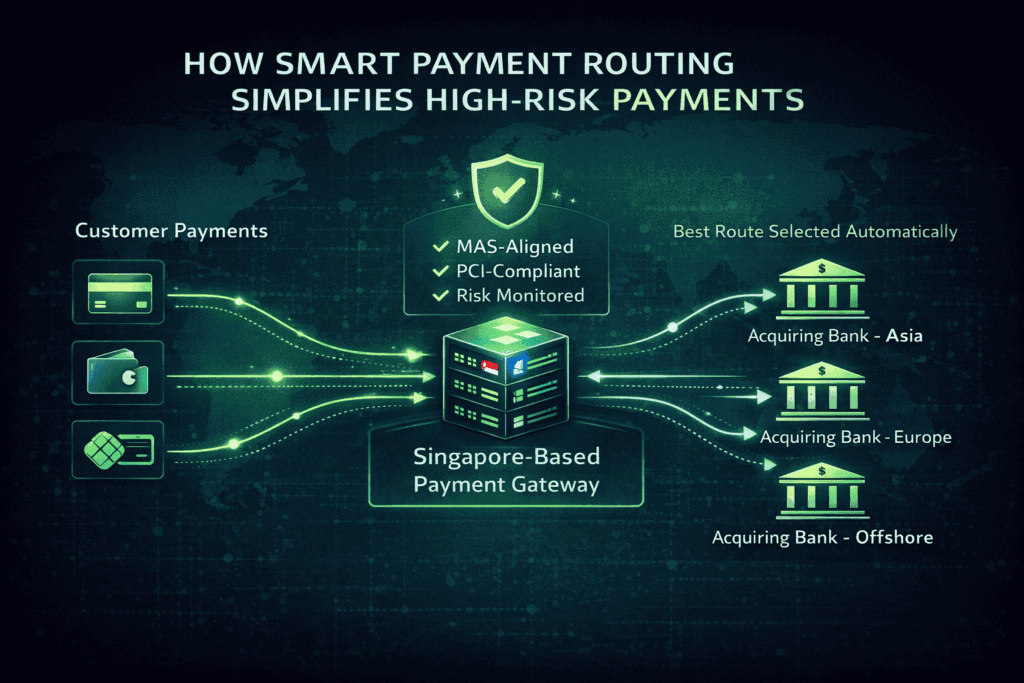

Diversifying merchant accounts across regions reduces dependency on any single acquiring relationship. Payment gateways with smart routing capabilities can dynamically direct transactions based on geography, risk signals, and performance thresholds.

At the same time, Alternative Payment Methods are becoming essential. Push-based options such as UPI, Pix, and regional wallets reduce chargeback exposure and complement traditional card-based high-risk payment solutions.

Conclusion

International high-risk payment processing as the industry approaches 2026 is defined by elevated cost, regulatory pressure, and operational complexity. Descriptor limitations, rolling reserves, automated enforcement, and AI-driven fraud are interconnected challenges rather than isolated problems.

Merchants that treat payments as a core element of risk management — rather than a background function — are better positioned to adapt. By diversifying acquiring relationships, protecting cash flow, and aligning compliance strategies across regions, businesses operating high-risk merchant accounts can move from reactive survival to sustainable global growth.

For merchants navigating high-risk payment processing across borders, choosing the right payment structure matters as much as the tools themselves. BoxCharge works with international merchants to align acquiring, compliance, and payment routing under a single framework.

Related Topics:

1: Why Banks De-Risk High-Risk Merchants — And How Businesses Can Survive It in 2026

2: Rolling Reserves Explained: How High-Risk Payment Processing Impacts Cash Flow

3: The Hidden Role of Correspondent Banks in Global Payment Failures

4: Chargebacks in High-Risk Businesses: The Hidden Role of Billing Descriptors

5: Fraud Detection Trends for 2026: How AI & Machine Learning Are Reshaping Payment Gateways

6: Visa Monitoring Programs (VAMP): High-Risk Merchant Risk & Compliance Guide