Built for gaming platforms that prioritize stability, compliance, and long-term account survivability.

Modern gaming platforms don’t fail because of volume. They fail because their payment infrastructure for gaming platforms wasn’t designed to survive growth.

For gaming operators, payment processing often looks deceptively simple at first. Players deposit, games run, payouts settle, and volume grows. Everything appears healthy — until one day it doesn’t.

Merchant accounts freeze. Reserves spike. Acquirers request “additional information.” In some cases, processing stops entirely with little warning.

What many operators learn too late is this:

Gaming merchant accounts rarely fail because of volume alone.

They fail because of player behavior patterns that conflict with how banks assess risk.

This article explains why gaming payment processing stability depends less on how much you process — and far more on how transactions behave over time.

Who This Is For

This article is written for gaming businesses that operate with scale, complexity, and long-term intent — not short-term experiments.

Specifically, it applies to:

- Platforms with recurring deposits or subscription mechanics

- Operators processing cross-border card volumes

- Businesses expanding into multiple jurisdictions

- Gaming models are subject to ongoing compliance oversight

- Merchants planning for sustained growth, not quick exits

By focusing on how businesses operate, rather than buzzwords like “casino” or “iGaming,” this approach mirrors how banks actually underwrite gaming merchant accounts.

The Real Problem: Why Accounts Fail After Approval

Most gaming merchant accounts don’t fail at onboarding.

They fail after growth begins.

That’s because approvals don’t break — risk models evolve.

Banks don’t review accounts once and forget about them. They continuously reassess transaction data using automated systems designed to detect changing risk profiles.

Three truths operators often underestimate:

- Banks react to patterns, not intent

- Growth triggers reviews

- Chargebacks are only one signal

A platform can stay published with chargeback thresholds and still face restrictions if transaction behavior shifts unexpectedly.

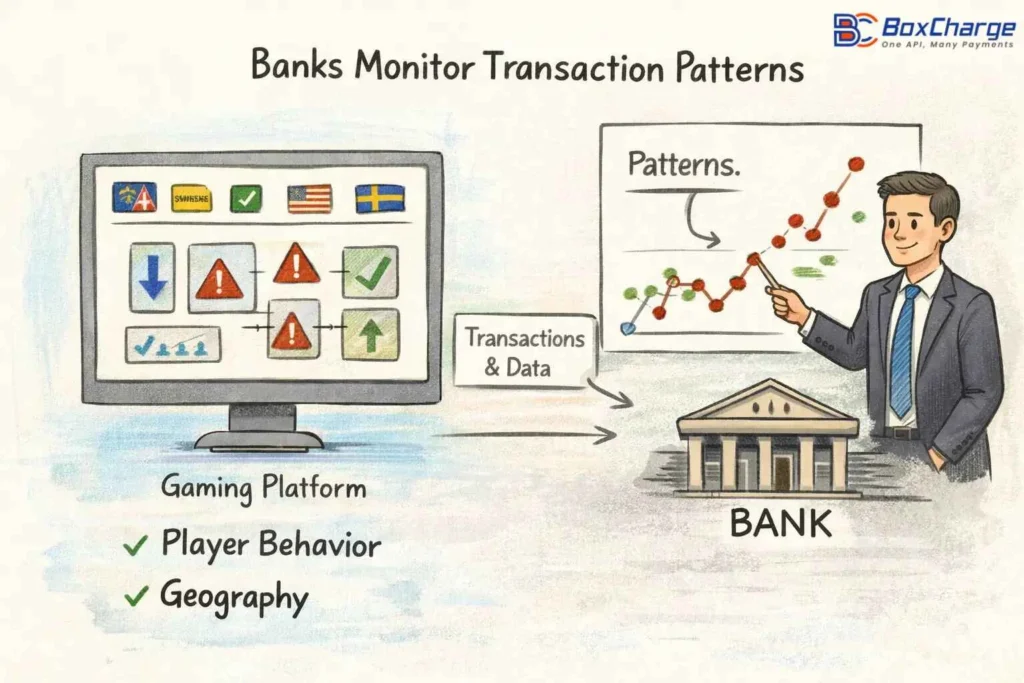

Why Player Behavior Matters More Than Volume

Platforms expanding into multiple jurisdictions often struggle with cross-border acquiring for gaming platforms, especially when domestic processors apply static risk rules.

From a bank’s perspective, volume is neutral.

Behavior is not.

Banks evaluate gaming transactions using pattern-based monitoring, including:

- Deposit frequency

- Ticket size changes

- Geographic spread

- Session clustering

- Dispute timing

A steady €500,000 monthly volume with predictable behavior is often considered safer than a sudden €100,000 spike with erratic activity.

How Banks Interpret Behavior

Banks don’t judge intent — they judge signals.

| Metric | Considered “Stable” | Considered “Risky” |

| Volume Growth | 10–15% MoM increase | 300% spike in 48 hours |

| Ticket Size | Consistent with gameplay | Sudden high-value deposits |

| Geography | Licensed regions | Rapid expansion into gray markets |

| Activity Timing | Even distribution | Clustered late-night bursts |

This is why operators often feel “punished for growing.”

In reality, they’re being flagged for unstructured growth.

Dispute Velocity: The Metric Most Operators Miss

Important:

Most operators don’t realize how banks assess gaming transaction behavior once volume patterns begin to shift. Most operators monitor their chargeback ratio (total disputes ÷ total transactions).Banks monitor dispute velocity — how many disputes hit within a short time window.

A sudden cluster of 8–10 disputes in 24 hours can trigger a settlement freeze faster than a 1% ratio spread over an entire month.

This is why many gaming merchant accounts are shut down even when headline metrics appear “within limits.”

Dispute velocity is one of the most common reasons stable-looking gaming businesses face sudden reviews.

How BoxCharge Solves This Problem

BoxCharge (high-risk payment gateway solutions provider) doesn’t sell shortcuts.

It designs payment structures that align with bank expectations from day one.

Rather than focusing on tools or buzzwords, the approach centers on predictability and reliability.

Key Principles

- Align transaction behavior with acquiring bank risk models

- Structure volume increases intentionally

- Monitor dispute velocity, not just ratios

- Design payment flows for continuous monitoring

How Dispute Velocity Is Managed

Without revealing proprietary systems, BoxCharge focuses on:

- Early velocity alerts

- Transaction pattern smoothing

- Geographic traffic alignment

- Adaptive routing logic

- Controlled escalation paths

The goal isn’t to eliminate risk.

It’s to make risk predictable.

Payment Infrastructure Overview

Stable platforms often rely on multi-MID payment structures and alternative payment rails to prevent sudden volume pressure on a single acquiring channel.

Gaming payment infrastructure should never be one-size-fits-all.

BoxCharge structures systems as modular components, allowing flexibility as the business evolves.

Infrastructure Components

- Gaming merchant accounts (single or multi-MID)

- International acquiring coverage

- Smart routing by region

- Alternative payment rails to balance card exposure

- Crypto settlement (optional, not mandatory)

This modular design allows operators to adapt without forcing volume through a single fragile channel.

Why Generic Processors Fail Gaming Merchants

Many low-risk processors don’t fail because they’re bad actors.

They fail because they’re structurally mismatched for gaming risk.

Common Gaps

- Low tolerance for behavioral variance

- Static fraud rules instead of adaptive monitoring

- Domestic routing for global traffic

- Fragmented underwriting communication

Gaming businesses require processors designed for complexity, not just transaction count.

Risk, Compliance & Long-Term Stability

A high-risk merchant account does not mean unmanaged.

BoxCharge operates within PCI-DSS-aligned environments, AML frameworks, and KYC protocols designed for regulated industries.

Key stability pillars include:

- Card network monitoring awareness

- Transparent dispute and refund handling

- Regulatory adaptability across regions

- Long-term account survivability focus

The objective is controlled exposure — not unrealistic promises.

Frequently Asked Questions

1: How long does approval take for a gaming merchant account?

Approval timelines vary by structure, geography, and risk profile. Most reviews are completed within a realistic underwriting window rather than instant approval claims.

2: Will reserves be required?

In most gaming models, yes. The focus is transparency — setting expectations early and structuring reserves predictably.

3: What happens if volume spikes suddenly?

Unstructured spikes can trigger reviews. Structured growth plans significantly reduce disruption. Yes, volume spikes are manageable when supported by real-time dispute pattern tracking and controlled international payment routing for gaming.

4: Is international traffic supported?

Yes. Through cross-border acquiring, BoxCharge supports regulated regions with aligned settlement structures.

5: What if the card pressure increases?

Alternative payment methods and routing adjustments can rebalance exposure without shutting down operations.

When This Solution Makes Sense

This structure works best for:

- Businesses planning sustained growth

- Operators prioritizing stability over speed

- Platforms willing to align behavior with bank models

It may not suit:

- Short-term projects

- Experimental traffic models

- Operators seeking guaranteed acceptance

Selective honesty builds stronger partnerships — with both merchants and banks.

Final Thought & CTA

Gaming payment stability isn’t about finding a processor that says “yes.”

It’s about building a structure that stays alive when scrutiny increases.

In just a few minutes, we’ll identify the three biggest risk triggers in your current payment flow — before they turn into freezes or reviews. Request a risk review.

Evaluate your payment readiness.

Discuss a scalable payment setup.