Scaling a Forex platform in 2026?

Most account freezes happen after approval.

A 15-minute Forex payment risk review can show where yours is exposed.

For many Forex brokers, getting a merchant account approved still feels like the biggest challenge.

In reality, approval is only the first checkpoint.

In 2026, the real risk isn’t rejection—it’s getting approved and then frozen once real trading activity begins. Funds held, settlements delayed, reserves increased, or entire accounts paused “pending review.”

This doesn’t happen because brokers are doing something illegal.

It happens because payment processing for Forex brokers is now evaluated continuously, not just at onboarding.

This guide explains how Forex merchant accounts are approved in 2026, what banks actually look for after approval, and how brokers can build forex trading payment solutions that stay live as volume grows—without sudden freezes.

Why Forex Merchant Account Approval Has Changed in 2026

Card networks and acquiring banks no longer treat Forex onboarding as a one-time decision.

Today, forex merchant account providers operate under live monitoring rules driven by:

- Cross-border transaction risk

- Dispute velocity (not just ratios)

- Deposit and withdrawal behavior

- Jurisdictional exposure

- Regulatory alignment

Approval is now a conditional starting point, not a finish line.

That’s why many brokers say:

“We were approved easily… and frozen 30–60 days later.”

What a Forex Merchant Account Really Is (and Isn’t)

A Forex merchant account is a high-risk payment processing arrangement designed to support:

- Forex trading deposits and withdrawals

- Ongoing client funding activity

- Cross-border forex payment processing

- Multi-currency settlement

- Regulatory oversight across regions

It is not a standard credit card merchant account.

Forex trading creates risk signals that banks treat differently:

- Funds are deposited before outcomes are known

- Market volatility affects refund behavior

- Disputes often come from confusion, not fraud

- Clients are international, not domestic

This is why payment processing for Forex brokers must be structured differently from day one.

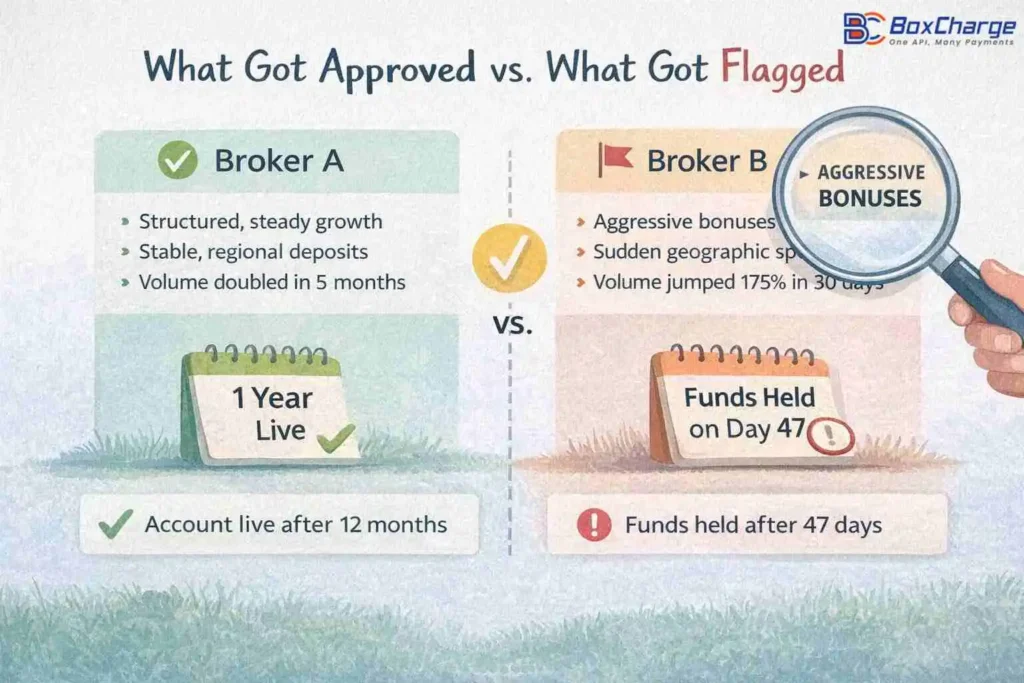

The #1 Reason Forex Merchant Accounts Get Frozen After Approval

Most brokers think freezes happen because of chargeback ratios.

Banks don’t think that way anymore.

They focus on behavioral signals, especially during the first 90 days:

- Sudden volume spikes

- Rapid geographic expansion

- Deposit sizes are increasing too quickly

- Withdrawal timing patterns

- Clusters of disputes in short windows

Approvals don’t fail. Risk models evolve.

If your live transaction data doesn’t match what was approved on paper, reviews begin automatically.

What Banks Actually Monitor in 2026 (Not What Brokers Expect)

One of the biggest misconceptions in Forex payment processing is that approval equals safety.

It doesn’t.

In 2026, banks and card networks don’t just assess what your business does — they continuously monitor how it behaves after going live. Most account freezes don’t happen because of fraud, but because real-time activity drifts outside the approved risk profile.

To make this clearer, here’s how acquiring banks typically classify Forex account behavior today:

How Banks Actually Score Forex Payment Risk in 2026

| Metric | “Safe” Operational Zone | “High-Risk” Review Trigger |

| Volume Growth | Structured, predictable 15–20% month-over-month growth | Unplanned 100%+ spike over a short period |

| Geographic Exposure | Traffic from pre-approved, declared regions | Sudden activity from non-core or restricted jurisdictions |

| Dispute Velocity | Evenly distributed disputes (around 1–2 per week) | Clusters of disputes (10+ within 48 hours) |

| Deposit Behavior | Consistent ticket sizes aligned with trading patterns | Sudden surge of high-value deposits without prior history |

| Billing Descriptor | Clear, recognizable, brand-aligned descriptor | Generic, unclear, or mismatched with website URL |

Important:

Most Forex brokers track chargeback ratios.

Banks track velocity, clustering, and behavioral change.

A short burst of unusual activity can trigger a review faster than a slow rise in ratios over time.

This is why many Forex merchant accounts remain stable for months — then suddenly face rolling reserves, payout delays, or temporary freezes when growth accelerates without structure.

Why This Matters for Forex Brokers Scaling in 2026

Forex trading payment solutions today are judged less on intent and more on pattern consistency.

When deposits, geographies, or transaction sizes change faster than the bank’s risk model expects, automated monitoring systems flag the account — often without warning.

This is especially common in:

- Cross-border Forex payment processing

- High-growth broker campaigns

- New trading platforms onboarding international clients

- Brokers offering multiple deposit methods without routing control

Without a payment structure designed for these scenarios, even compliant brokers can face interruptions.

This is exactly where specialized Forex merchant account providers like BoxCharge focus — not just on approval, but on post-approval survivability.

How BoxCharge Aligns Forex Payment Behavior With Bank Expectations

Rather than reacting after a review happens, BoxCharge works upstream by helping brokers:

- Structure volume increases intentionally

- Align billing descriptors with brand and domain signals

- Control dispute velocity before it clusters

- Route cross-border Forex transactions through appropriate acquiring paths

The goal isn’t to suppress growth — it’s to ensure growth stays predictable, explainable, and review-safe.

Because in Forex payment compliance, stability isn’t about avoiding risk.

It’s about making risk visible, measurable, and controlled.

Forex Payment Compliance: What Banks Actually Monitor

In 2026, forex payment compliance is about predictability, not perfection.

Banks monitor:

- Transaction pacing (how fast volume grows)

- Deposit-to-withdrawal ratios

- Country-level exposure consistency

- Descriptor clarity on statements

- Retry behavior after declines

Even brokers with clean compliance records get frozen when growth looks unstructured.

This is why secure forex payments aren’t just about fraud tools—they’re about how activity unfolds over time.

Case Example: Approved, Then Frozen (And What Changed)

A mid-size Forex broker we worked with launched using a newly approved forex broker payment gateway.

Initial setup:

- EU-focused onboarding

- €25k–€40k monthly volume projection

- Clean compliance documentation

What happened:

- Influencer campaign performed better than expected

- Volume jumped 220% in 30 days

- New deposits came from 6 additional countries

- Withdrawal timing stayed unchanged

Nothing illegal. Nothing deceptive.

Yet settlements were frozen pending review.

Why?

The growth curve no longer matched the approved risk profile.

The Fix

We restructured:

- Gradual country enablement

- Deposit limits aligned with account age

- Split routing for higher-risk geographies

- Clearer billing descriptors and reminders

Within weeks, settlements resumed—without changing the business model.

That’s the difference between forex transaction processing and risk-aware forex payment architecture.

How to Get a Forex Merchant Account Approved (and Keep It Live)

Approval in 2026 depends on how well your setup answers one question:

“Can this broker grow without surprising the bank?”

1. Choose the Right Forex Merchant Account Providers

Avoid processors that specialize in low-risk ecommerce.

You need providers that understand:

- Forex trading deposits and withdrawals

- Regulatory overlap across regions

- Ongoing monitoring, not just onboarding

Generic gateways approve quickly—and freeze faster.

2. Design Cross-Border Forex Payment Processing Intentionally

Banks dislike sudden geographic expansion.

Instead:

- Launch with defined regions

- Enable countries in phases

- Match traffic sources with approved geos

This shows control, not chaos.

3. Structure Deposits and Withdrawals from Day One

Unbalanced flows trigger scrutiny.

Best practices:

- Avoid large early deposits

- Introduce tiered funding limits

- Maintain consistent withdrawal windows

This stabilizes payment solutions for trading platforms under monitoring.

4. Treat Dispute Velocity as a Risk Metric

Most brokers track dispute ratios.

Banks track how fast disputes appear.

Ten disputes in 48 hours raise more alarms than a 0.8% monthly ratio.

Managing velocity means:

- Clear onboarding explanations

- Descriptor clarity

- Timely withdrawal communication

This is central to secure forex payments.

Payment Infrastructure That Survives Growth

Successful brokers don’t rely on a single rail.

Modern forex trading payment solutions often include:

- Multiple merchant accounts (MIDs)

- Regional acquiring

- Smart routing by geography

- Alternative payment methods for balance

- Optional crypto settlement where compliant

This isn’t complexity—it’s stability.

Why Many Forex Broker Payment Gateways Fail at Scale

Most failures aren’t technical.

They’re structural.

Common issues:

- Static risk rules

- No continuity between underwriting and monitoring

- Domestic rails forced onto global businesses

- Low tolerance for behavioral change

Forex requires adaptive payment processing, not fixed assumptions.

Regulatory Reality: Licensing Still Matters

Licensing doesn’t guarantee approval—but it helps shape trust.

Easier jurisdictions:

- Some EU frameworks (with substance)

- Select offshore regions with strong reporting

Harder jurisdictions:

- Light-touch licenses with poor transparency

- Mismatch between license and client geography

Banks look at:

- License credibility

- Operational substance

- Ongoing reporting discipline

Forex payment compliance is as much operational as legal.

Frequently Asked Questions

1: How long does Forex merchant account approval take in 2026?

Typically 7–15 business days, depending on structure and geography.

2: Should brokers expect rolling reserves?

Yes. The focus should be on how reserves are released, not whether they exist.

3: Can you support international traders?

Yes. Cross-border forex payment processing is essential for modern brokers.

4: What if trading volume spikes?

Planned growth is manageable. Unplanned spikes trigger reviews.

5: Are alternative payment methods useful?

Yes—when used strategically to balance card exposure.

When This Approach Makes Sense (and When It Doesn’t)

Best for:

- Brokers planning long-term growth

- Platforms prioritizing payment stability

- Regulated or compliance-aware teams

Not ideal for:

- Short-term launches

- Arbitrage-driven traffic spikes

- “Approve first, figure it out later” models

Being selective protects everyone involved.

Final Thoughts

Getting a Forex merchant account approved in 2026 is no longer the challenge.

Keeping it live is.

Forex businesses don’t fail because they’re risky.

They fail because their payment foundations weren’t built for success.

Approval is procedural.

Stability is engineered.

Request a Forex Payment Risk Review, before volume growth forces a review you didn’t plan for

If you’re launching—or scaling—a Forex platform and want to know whether your current payment processing for Forex brokers can survive real growth:

We’ll review your setup, traffic model, and transaction behavior

before problems appear.

That’s how serious Forex platforms stay operational in 2026.