Okay, so imagine this scenario:

A customer browses your adult subscription site, enters their card details, and happily completes a payment. A few weeks later, that same cardholder opens their bank statement, sees a line they don’t immediately recognize, and hits “Dispute.”

Suddenly, your payments slow. Settlements pause. Your acquiring bank asks for more documentation. Within a few billing cycles, your merchant account is under review — even though your pricing, compliance, and marketing were all above board.

What went wrong?

Not your traffic.

Not your content.

Not even your conversion numbers.

It was your descriptor strategy — the language banks and customers see on credit card statements — and the way it influences how transactions are recognized and interpreted long after the sale.

In the complex world of high-risk payment processing, descriptor clarity can make or break your adult merchant account. This blog explores why billing descriptors matter globally, how financial institutions view them, and how adult businesses can build payment infrastructure that survives not just today’s scrutiny — but the evolving standards of 2026 and beyond.

The Global Context: Why Adult Merchant Accounts Are High-Risk

Across regions, adult businesses are considered high-risk by acquiring banks and payment processors. This isn’t a moral judgment — it’s about financial risk and regulatory uncertainty.

Banks and processors often decline adult merchant applications because of:

- High expected chargeback rates, especially for subscription or digital services, where content recognition fades over time.

- Reputational risk, where associations with adult services are viewed unfavorably by wider banking partners.

- Regulatory complexity, with different laws governing adult content, age verification, and payment disclosure across jurisdictions.

Even in markets with more permissive adult content laws (e.g., parts of Europe or Latin America), banks are cautious because:

- Compliance frameworks like GDPR and PSD2 introduce rigorous payment authentication and data rules

- Issuers require clear age verification and content legality

- Chargeback management expectations are higher than for typical e-commerce

This means that adult merchant accounts are usually issued as high-risk merchant accounts, and only through payment partners who specialize in these industries.

Licensing and Regulatory Barriers Around the World

If you want to accept payment online at scale for adult content or services, having the right merchant account isn’t optional — it’s foundational. But where and how you do it affects not just approval chances, but your long-term stability.

1: North America (USA & Canada)

In the United States, adult merchant accounts face layered regulatory expectations:

- Banks and payment processors will dig into business details to ensure compliance with local and federal laws, including age verification and clear refund policies.

- Major card schemes (e.g., Mastercard) have additional requirements for adult content merchants, including age/identity verification and content monitoring if your site includes user-generated material.

- Traditional low-risk gateways (Stripe, PayPal, Square) nearly universally prohibit adult content, leaving only high-risk specialists.

Approval timelines and requirements can vary:

- Standalone adult sites with strong documentation may get approved in days at specialist institutions

- New marketplace models or adult platforms without a processing history may face months of review and tighter conditions

Approval can be relatively easier with specialist high-risk payment partners if documentation, compliance, and descriptor strategy are strong. However, without proper compliance and age verification, accounts will probably be rejected or shut down.

2: Europe

In EU markets, adult content is legal in most countries, but financial services still classify the industry as high risk:

- PCI-DSS frameworks apply rigorously

- Strong Customer Authentication (SCA) and PSD2 add layers of compliance

- Age verification and content legality are important to avoid liability

European banks are typically more flexible than their U.S. counterparts, but they still require:

- Proof of legal age and content ownership

- Transparent refund and billing policies

- Clear anti-money-laundering (AML) practices

3: Latin America, APAC, and Other Regions

These regions vary widely in regulatory rigor:

- Latin America has a growing e-commerce ecosystem, but still places adult content in the high-risk bucket for financial services.

- Some APAC countries have strict telecommunication and content laws that ripple into payment approval expectations

In many of these markets, local licensing isn’t required for adult content itself, but payment processors still impose documentation and compliance thresholds similar to those in the U.S. and EU before approving high-risk merchant accounts.

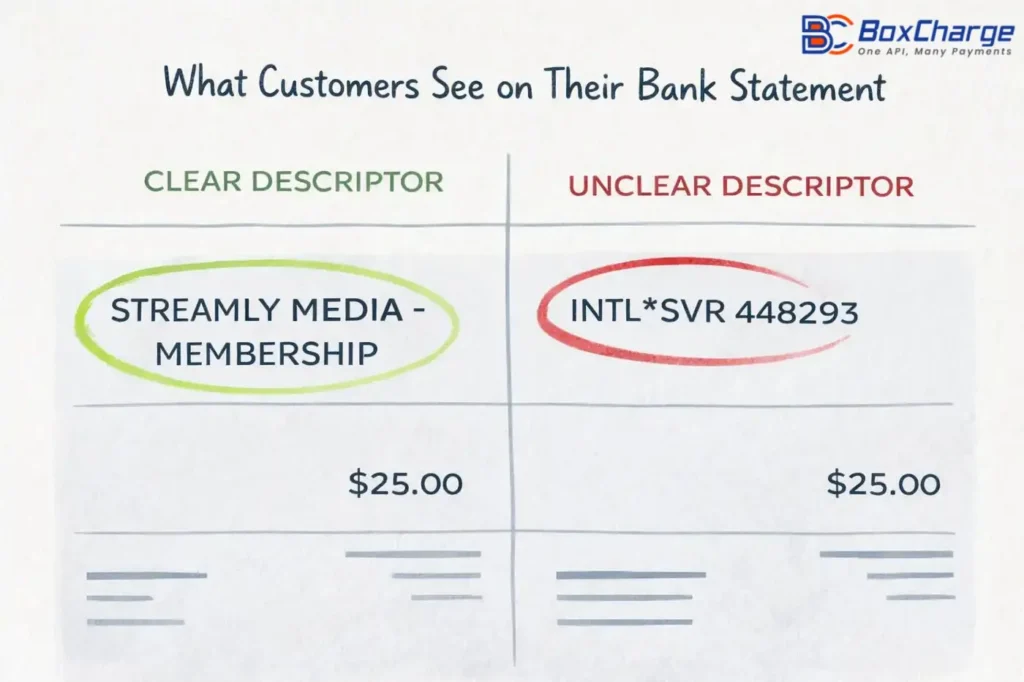

Descriptor Strategy: Why It’s Now a Bank-Level Concern

When people think of billing issues, they usually think of chargebacks or refunds. Banks think differently.

To an issuing bank, the descriptor isn’t a branding choice. It’s a risk signal.

Here’s why:

1: Customer Recognition

If a cardholder doesn’t immediately recognize what they paid for — even weeks later — they are far more likely to dispute the charge.

These “unrecognized charges” rank high among adult merchant disputes.

2: Issuer Interpretation

Issuers use descriptors as metadata. Confusing or generic lines (e.g., “PAYMENT *12345”) don’t tell the bank or the cardholder anything about the transaction context. This increases ambiguity, and ambiguity always increases risk scores.

3: Pattern Monitoring

Banks don’t focus on static ratios. They monitor:

- Dispute velocity (clustering over time)

- Descriptor clarity trends

- Refund vs dispute timing

…all of which inform how the risk model evolves post-approval.

Ten disputes clustered in 48 hours often trigger a risk review faster than a small percentage of disputes spread out evenly.

A Real Example: How Descriptor Confusion Triggers Reviews

Consider two subscription-based adult platforms:

Platform A:

Accepts payments with a descriptor that matches the domain, product context, and confirmation email copy. Cardholders recognize charges even weeks later.

Platform B:

Uses a generic payment label that barely resembles the brand or purchase context.

Even if both have identical volumes and ratios, Platform B will attract more “unrecognized charge” disputes, leading to:

- Early monitoring alerts

- Manual review requests from banks

- Increased likelihood of rolling reserves or holds

This pattern is one of the most common reasons stable adult accounts encounter freezes or rolling reserves.

Descriptor Design Is Infrastructure — Not Creative Copy

Many merchants treat descriptors as a branding decision or a marketing detail. In reality, the descriptor strategy must be embedded into your payment architecture.

A strong descriptor approach considers:

- Domain alignment (the billing name should match the website domain)

- Purchase context language (e.g., terms used during checkout)

- Local and international variations (descriptor presentation may differ by region)

- Customer support workflows that reference the exact descriptor

Platforms that connect descriptor design with confirmation emails, user dashboards, and customer support scripts drastically reduce unrecognized disputes.

This becomes even more important in high-risk categories like online merchant accounts, online dating merchant accounts or casino merchant accounts, where ambiguity increases dispute probability.

What It Takes to Adult Merchant Account Approved

Approval is no longer a checkbox. It’s a multi-factor verification that blends compliance, documentation, and descriptor clarity.

1: Documentation and Operational Proof

Banks will ask for:

- Business formation documents

- Operating licenses (if required by your jurisdiction)

- Age verification and content control policies

- Tax and corporate registration

- Website and domain ownership verification

2: Compliance and Risk Controls

To get approved — and stay approved — you need:

- PCI-DSS compliance

- Clear refund and dispute handling policies

- Age verification mechanisms

- Anti-money-laundering (AML) and KYC frameworks

Lacking any of these often results in:

- Higher fees

- Rolling reserves

- Declined applications

3: Choosing the Right Partner

Mainstream processors like PayPal, Stripe, or Square are effectively off-limits for adult merchants — they often shut accounts once they discover the business type.

This means you must work with:

- High-risk merchant account solutions providers

- Adult-friendly acquiring banks

- Global payment gateways with high-risk underwriting expertise

These partners understand how to frame descriptors, compliance documentation, and legal context in a way that meets bank and card scheme expectations.

FAQ: Pain Points Adult Merchants Face

1: How long does approval take?

Depending on documentation and jurisdiction, it can range from a few days to several weeks — significantly slower than low-risk setups.

2: Is a license always required?

Not always for content itself, but regulatory compliance (age verification, privacy policy, refunds) is mandatory in most markets and impacts approval outcomes.

3: Can descriptor clarity actually prevent disputes?

Yes. A thoughtful descriptor reduces confusion and lowers the likelihood of “unrecognized charge” disputes.

4: What about alternative payment methods?

Diversifying with wallets and crypto options can reduce reliance on card rails and mitigate risk exposure.

Final Insight

Most adult merchant accounts fail not because the business is flawed, but because payments are not engineered for recognition.

Approval is a starting point.

Stability comes from clarity.

If your credit card merchant account is built around ambiguity, you are building on sand.

What to Do Next

If you’re operating or planning to operate an adult business and want to evaluate whether your payment strategy — including descriptor design, compliance, and structural readiness — can survive real growth, BoxChrge can help.

In a small time, we’ll identify the three biggest risk triggers affecting your payment setup.

No hype. Just preparation.