A Forex merchant account is essential for brokers accepting client deposits, but most Forex merchant accounts get shut down within 90 days due to how banks monitor risk after approval.

For many Forex brokers, getting a merchant account approved feels like crossing the hardest hurdle.

In reality, approval is only the beginning.

• Most Forex merchant accounts fail after approval—not before

• Growth, not fraud, triggers reviews

• Banks monitor behavior patterns, not promises

• Stable payment infrastructure determines account survival

What most platforms discover—often too late—is that the real test starts after transactions go live. As volume grows, payment behavior changes. Banks reassess risk. Monitoring systems recalibrate. And accounts that looked “approved” suddenly face freezes, rolling reserves, or outright termination within the first 60 to 90 days.

This isn’t about bad actors or broken rules.

It’s about a payment infrastructure that wasn’t designed to survive growth.

At BoxCharge, we work with Forex businesses that can’t afford interruptions—businesses where payments aren’t just operational, they’re existential. This article explains why Forex merchant accounts fail early, what banks actually react to, and how a risk-aware payment structure keeps accounts live long after launch.

What Is a Forex Merchant Account?

A Forex merchant account is a specialized payment processing arrangement that enables Forex brokers and trading platforms to accept client deposits through cards and alternative payment methods, while operating under elevated risk oversight from banks and card networks.

Unlike standard merchant accounts, a Forex merchant account is underwritten specifically for trading activity, cross-border flows, and dispute-heavy environments. It is designed not only to process payments but to remain operational as volume, geography, and regulatory exposure increase.

For Forex businesses, this account is not optional infrastructure.

It is the foundation that determines whether payments remain live or get interrupted once real trading activity begins.

Why Forex Merchant Accounts Are Classified as High-Risk

High-risk forex businesses are classified by banks due to structural factors, not intent.

These include:

- Client funds are deposited before outcomes are realized

- Market volatility influences refund and dispute behavior

- A higher-than-average chargeback probability

- Heavy cross-border card usage

- Ongoing regulatory review across jurisdictions

As a result, Forex merchant accounts are subject to continuous monitoring after approval, not just at onboarding.

This is where many platforms struggle—not because of non-compliance, but because their payment setup was never built for sustained scrutiny, because their Forex payment processing setup was never built for sustained scrutiny.

How a Forex Merchant Account Differs From a Regular Merchant Account

A regular merchant account is built for predictable, low-risk transactions.

A Forex merchant account is built for complexity.

Key differences include:

- Stricter underwriting requirements

- Ongoing monitoring after approval

- Rolling reserves or delayed settlements

- Lower tolerance for sudden volume changes

- Higher expectations around dispute handling and refunds

This is why many Forex platforms get approved easily—but struggle to stay live once real transaction data starts flowing.

The Role It Plays in Long-Term Stability

A properly structured Forex merchant account isn’t just a payment tool.

It’s part of your risk management strategy.

When designed correctly, it helps:

- Maintain settlement continuity

- Reduce unexpected freezes

- Align growth with bank expectations

- Support expansion into new markets without triggering reviews

In short, a Forex merchant account doesn’t guarantee success—but without the right one, sustainable growth is nearly impossible.

Payment Stability Matters More Than Fast Approval

In Forex, speed is often mistaken for strength.

Fast approvals, low documentation, and “instant onboarding” may look attractive—but they rarely hold up once real volume starts flowing. Banks don’t reward speed. They reward predictability.

What they want to see is simple:

- Controlled transaction behavior

- Gradual, explainable growth

- Dispute patterns that stay within expectations

- Infrastructure that adapts as risk evolves

Payment systems built for stability—not hype—are the ones that survive.

That’s why serious Forex businesses prioritize infrastructure designed to stay live as volume grows, not shortcuts that collapse under scrutiny.

Who This Is For

This article isn’t for experimental trading apps or short-term projects. It’s for Forex businesses that operate at scale—or are preparing to.

Specifically, this applies to:

- Platforms with recurring billing or funded accounts

- Forex brokers processing cross-border card volumes

- Businesses expanding into multiple jurisdictions

- Models operating under regulatory or compliance pressure

- Teams planning for growth, not just launch

By focusing on how businesses operate—not just what they sell—this distinction matters to banks, card networks, and Google alike.

The Real Problem: Why Accounts Fail After Approval

Forex merchant accounts don’t usually fail because of fraud.

They fail because risk models change once real data appears.

Here’s what typically happens.

Approvals Don’t Fail—Risk Models Evolve

At the approval stage, banks assess projected risk.

Once transactions begin, they assess actual behavior.

Volume spikes, geographic expansion, and user behavior patterns trigger new evaluations—often automatically.

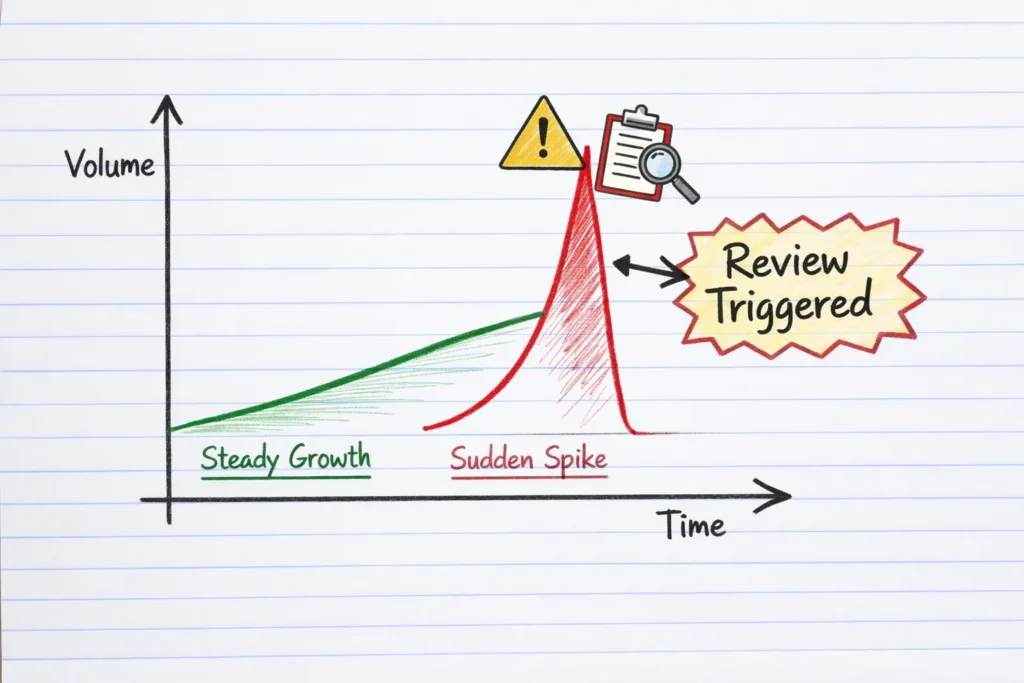

Growth Triggers Reviews

An account processing $20,000 per month behaves very differently from one processing $200,000.

Sudden increases in:

- Transaction frequency

- Ticket size

- Country mix

- Payment method usage

All signal change—and change attracts scrutiny.

Chargebacks Aren’t the Only Signal

Many merchants fixate on chargeback ratios. Banks don’t.

They also monitor:

- Dispute velocity (how fast disputes accumulate)

- Refund timing

- Retry behavior

- Issuer decline patterns

- Cross-border approval consistency

Banks react to patterns, not intent. Even well-run Forex platforms get flagged when growth isn’t structured.

A Real Story: Approved, Then Frozen

One Forex brokerage we worked with launched with a clean setup and passed underwriting smoothly.

Within 45 days, their user base grew faster than expected.

Volume doubled. International traffic increased. Refund timing stayed the same.

On paper, nothing was “wrong.”

But the bank froze settlements pending review.

Why?

Because the growth curve didn’t match the original risk profile.

The issue wasn’t fraud—it was unstructured success.

This pattern is something we’ve seen repeatedly across multiple Forex platforms during early-stage scaling.

How BoxCharge Structures Forex Merchant Accounts for Long-Term Stability

At BoxCharge, we don’t focus on tools—we focus on behavior alignment.

Our approach is built around predictability.

Aligning Transaction Behavior With Bank Expectations

Banks don’t need perfection. They need consistency.

We help structure:

- Transaction pacing

- Geographic exposure

- Payment method distribution

- Refund and dispute workflows

so that growth looks intentional—not erratic.

Designing Volume Increases Intentionally

Instead of letting volume spike naturally (and dangerously), we guide controlled scaling that aligns with underwriting assumptions.

This protects:

- Settlement continuity

- Merchant account longevity

- Banking relationships

Managing Dispute Velocity, Not Just Ratios

Two merchants can have the same chargeback ratio. One gets shut down. One doesn’t.

The difference is how disputes appear over time.

We design payment flows that reduce sudden dispute clustering—one of the most overlooked risk factors in Forex processing.

For Forex businesses already processing live volume, early payment structure decisions often determine whether accounts stay operational.

A structured risk review can reveal whether your current setup aligns with how banks evaluate growth.

Payment Infrastructure: Built-in Components, Not Promises

Forex businesses don’t need one rigid system. They need a modular infrastructure that adapts as risk changes.

A mature setup may include:

- Single or multiple merchant accounts (MIDs)

- International acquiring across regions

- Smart transaction routing by geography

- Alternative payment rails to balance volume

- Optional crypto settlement where appropriate—not mandatory

This flexibility signals operational maturity to banks and card networks.

Why Generic Processors Fail Forex Businesses

Most low-risk processors don’t fail because they’re incompetent.

They fail because they’re structurally mismatched.

Common issues include:

- Low tolerance for dispute fluctuations

- Static fraud rules that don’t adapt

- Forcing global businesses through domestic rails

- No continuity between the underwriting and monitoring teams

Forex requires systems designed for complexity, not just throughput.

Risk, Compliance & Long-Term Stability

In Forex, the goal isn’t to eliminate risk.

That’s impossible.

The goal is to make risk predictable.

This means:

- Awareness of card network monitoring programs

- Transparent handling of disputes and refunds

- Regulatory adaptability across regions

- Long-term survivability over short-term gains

Banks respect merchants who understand this distinction.

Frequently Asked Questions

1: What is the typical approval timeline for a Forex merchant account?

Realistic timelines range from 5 to 15 business days. This allows for deep-dive underwriting into your corporate structure and risk profile.

2: Why do banks require rolling reserves for Forex processing?

Yes, reserves are standard for high-risk trading platforms. They act as a security buffer against market volatility and potential chargebacks.

3: Does BoxCharge support cross-border Forex deposits for global traders?

Absolutely. Our infrastructure is built specifically for international acquiring, allowing you to accept payments from multiple jurisdictions without triggering fraud blocks.

4: How does sudden volume growth affect Forex merchant account stability?

Unplanned spikes often trigger automatic bank freezes. We manage this by designing controlled scaling paths that align with bank expectations before the growth happens.

5: How can I reduce my platform’s dependency on card-only deposits?

We design “multi-rail” strategies, integrating alternative payment methods (APMs) and smart routing to ensure your platform stays live if card networks tighten restrictions.

When This Solution Makes Sense And When It Doesn’t

This approach works best for:

- Forex businesses planning to scale

- Teams prioritizing stability over speed

- Models built for long-term operation

It is not ideal for:

- Short-term projects

- Experimental launches

- Businesses chasing instant approval without structure

Being selective isn’t exclusionary—it’s responsible.

Final Thoughts

Most Forex merchant accounts don’t fail because the business is flawed.

They fail because the payment foundation wasn’t built to survive success.

Approval is easy.

Stability is engineered.

Request a Risk Review With BoxCharge

If you’re operating—or planning to operate—a Forex business and want to understand whether your payment setup can survive real growth, we’ll start with an honest assessment.

Request a risk review.

We’ll evaluate your payment readiness before anything else—and tell you if this structure fits your business.

That’s how serious growth begins.