Looking for the best offshore merchant account for your high-risk business? Choosing between an offshore and a domestic merchant account can significantly affect your approval rate, payment stability, international growth, and overall revenue. For businesses operating in high-risk industries, selecting the wrong payment solution can result in declined applications, frozen funds, high chargeback fees, and even sudden account termination.

If you've spent weeks searching for a reliable payment processor only to receive rejection after rejection, you're not alone. Thousands of legitimate businesses struggle to secure payment processing simply because they operate in industries that banks classify as high risk. Whether you're running an IPTV platform, online gaming website, travel agency, forex brokerage, nutraceutical brand, CBD business, subscription service, or digital marketplace, finding the right merchant account is often more difficult than acquiring customers.

This is where understanding the difference between offshore merchant accounts and domestic merchant accounts becomes essential.

While domestic merchant accounts are ideal for many low-risk businesses serving local customers, offshore merchant accounts are specifically designed to support businesses with international customers, recurring billing, higher chargeback risks, and complex business models.

In this comprehensive guide, we'll explain the differences between offshore and domestic merchant accounts, compare their advantages and disadvantages, highlight the challenges high-risk merchants face, and help you choose the right payment solution to support long-term business growth.

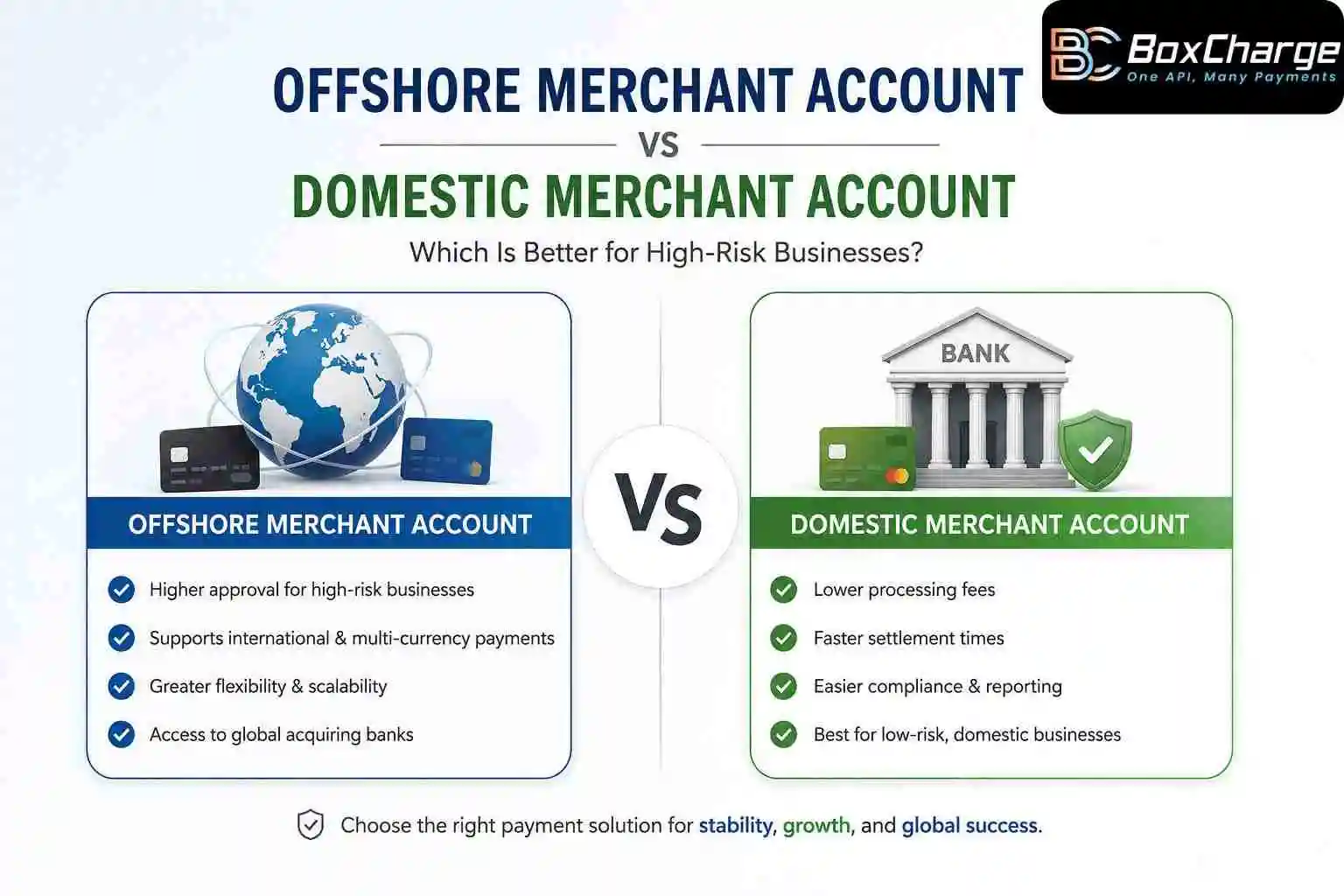

Offshore Merchant Account vs Domestic Merchant Account: Side-by-Side Comparison

If you're looking for a quick answer, here's how the two compare.

Feature | Offshore Merchant Account | Domestic Merchant Account |

Best for High-Risk Businesses | ✅ Yes | ⚠️ Limited |

Approval Rate | Higher | Lower |

International Payments | Excellent | Limited |

Multi-Currency Processing | Yes | Often Limited |

Chargeback Flexibility | Better | Strict |

Cross-Border Transactions | Optimized | Limited |

Settlement Speed | Moderate | Faster |

Processing Fees | Slightly Higher | Usually Lower |

Business Scalability | Excellent | Moderate |

Why Choosing the Right Merchant Account Matters

For a traditional retail store, switching payment providers is usually a simple operational decision.

For a high-risk business, it's often a business survival decision.

One rejected application can delay your launch. One frozen settlement can disrupt payroll. One terminated merchant account can instantly stop revenue from flowing into your business.

Unfortunately, these situations are common because many acquiring banks evaluate businesses based on perceived risk rather than operational quality.

A legitimate business with excellent customer service can still struggle to obtain payment processing simply because it operates in a high-risk Merchant Category Code (MCC).

That's why selecting the right merchant account isn't just about transaction fees—it's about finding a provider that understands your industry and supports your long-term growth.

What Is a Merchant Account?

A merchant account is a specialized business account that enables companies to accept credit card and debit card payments online or in person. When a customer makes a payment, the funds are temporarily held by the acquiring bank before being transferred to the business's bank account.

Merchant accounts work alongside payment gateways to securely authorize, process, and settle card transactions.

Without a merchant account, businesses cannot accept Visa, Mastercard, or other major card payments efficiently.

What Is a Domestic Merchant Account?

A domestic merchant account is issued by a bank or payment processor located in the same country where your business is legally registered.

For example:

A UK business working with a UK acquiring bank

A Singapore company processing payments through a Singapore bank

A Canadian merchant using a Canadian payment processor

Domestic merchant accounts are designed primarily for businesses that serve customers within their local market and operate in industries considered low to moderate risk.

Benefits of a Domestic Merchant Account

A domestic merchant account offers several advantages for businesses with stable risk profiles.

1: Lower Processing Costs

Domestic transactions generally involve fewer intermediaries, resulting in lower processing fees.

2: Faster Settlement Times

Payments often settle more quickly because transactions remain within local banking systems.

3: Simplified Compliance

Working with domestic financial institutions makes tax reporting, reconciliation, and regulatory compliance easier.

4: Local Customer Trust

Customers are often more comfortable making payments through familiar domestic banking networks, improving confidence during checkout.

Why High-Risk Businesses Often Struggle with Domestic Merchant Accounts

This is where many businesses encounter problems.

Traditional banks prioritize risk reduction. If your industry has historically experienced higher rates of fraud, chargebacks, or regulatory scrutiny, approval becomes significantly more difficult.

Some of the most common reasons domestic payment providers reject applications include:

1: High Chargeback Ratios

Chargebacks represent financial risk for acquiring banks. Businesses offering subscriptions, digital services, or international transactions naturally experience higher dispute rates, making banks more cautious.

2: Cross-Border Payment Business Models

Selling to customers in multiple countries introduces additional fraud prevention requirements, currency conversions, and compliance obligations.

Many domestic providers simply choose not to support these businesses.

3: Recurring Billing

Subscription-based businesses frequently face payment disputes due to forgotten renewals, expired cards, and customer misunderstandings.

While recurring revenue is valuable for businesses, it increases perceived risk for payment providers.

4: Industry Classification

Many legitimate industries are automatically categorized as high risk, including:

IPTV services

Forex trading

Online gaming

Adult entertainment

Travel agencies

CBD products

Nutraceutical supplements

Digital marketing agencies

Ticketing platforms

Subscription businesses

Being classified as high risk doesn't mean your business is unsafe—it simply means banks require additional risk management before approving payment processing.

What Is an Offshore Merchant Account?

An offshore merchant account is a merchant account provided by an acquiring bank located outside the country where your business is incorporated.

Unlike many domestic providers, offshore acquiring banks often specialize in supporting international businesses and industries that traditional financial institutions consider high risk.

These providers understand that not every high-risk merchant is a risky business.

Instead of rejecting applications solely based on industry type, they evaluate factors such as processing history, financial stability, fraud prevention measures, business operations, and compliance practices.

For businesses expanding internationally, offshore merchant accounts also provide access to multi-currency payment processing, global acquiring networks, and broader card acceptance, making them a practical choice for long-term growth.

Why Offshore Merchant Accounts Are the Preferred Choice for High-Risk Businesses

For many high-risk businesses, an offshore merchant account isn't just another payment processing option—it's often the only realistic way to accept credit card payments consistently.

Unlike traditional banks that follow strict underwriting guidelines, offshore acquiring banks are generally more experienced in evaluating businesses with complex payment requirements. They understand that industries with higher chargebacks or international customers are not necessarily fraudulent; they simply require a different risk management approach.

Let's explore the biggest advantages.

1. Higher Approval Rates

Perhaps the biggest reason merchants choose offshore acquiring is the significantly higher approval rate.

Domestic banks often reject applications before reviewing the business in detail simply because of the Merchant Category Code (MCC). Offshore providers typically perform a more comprehensive evaluation, considering factors such as:

Processing history

Average monthly sales

Business model

Chargeback ratio

Fraud prevention measures

Website compliance

Financial stability

This approach gives legitimate businesses a much better chance of securing a reliable merchant account.

2. Better Support for International Payments

If your customers are located in different countries, payment processing becomes far more complex.

An offshore merchant account is designed to handle:

International credit card payments

Cross-border transactions

Multiple acquiring banks

Global payment acceptance

Currency conversion

International settlement

Instead of limiting your growth, offshore payment processing helps your business expand into new markets with fewer payment restrictions.

3. Multi-Currency Payment Processing

Modern consumers prefer paying in their local currency.

Offshore merchant accounts often support:

USD

EUR

GBP

SGD

AUD

CAD

AED

And many other global currencies

Displaying prices in the customer's preferred currency improves trust, reduces cart abandonment, and creates a better checkout experience.

4. Greater Scalability

Many businesses begin with domestic payment processing but quickly outgrow their provider.

As transaction volume increases, domestic processors may introduce:

Processing caps

Reserve increases

Additional underwriting

Delayed settlements

Higher scrutiny

Offshore acquiring partners are generally better equipped to support growing businesses with larger transaction volumes and international customer bases.

5. Better Support for Subscription Businesses

Recurring billing remains one of the biggest challenges for domestic payment providers.

Businesses offering memberships, SaaS products, streaming platforms, coaching programs, or subscription services frequently experience:

Expired payment methods

Customer disputes

Friendly fraud

Chargebacks

Offshore merchant accounts are often better suited for recurring payment models because they are designed to accommodate these risks through stronger fraud controls and flexible underwriting.

The Hidden Costs of Choosing the Wrong Merchant Account

Many businesses focus only on processing fees when comparing providers.

This is often a costly mistake.

Saving 0.30% on transaction fees means very little if your account is suddenly terminated during your busiest sales period.

The real costs include:

Lost revenue from payment interruptions

Customer frustration during failed transactions

Delayed settlements are affecting cash flow

Additional compliance reviews

Time spent searching for replacement providers

Damage to your brand reputation

Payment stability should always carry more weight than small differences in transaction pricing.

Common Problem High-Risk Merchants Face

Every week, businesses approach payment providers after facing similar challenges.

"Our Application Was Rejected Without Explanation"

Many acquiring banks decline applications based purely on industry classification, leaving merchants with no clear understanding of what went wrong.

"Our Funds Were Frozen"

Nothing disrupts business operations faster than frozen settlements.

Without access to working capital, businesses struggle to pay suppliers, employees, advertising platforms, and operational expenses.

"Our Payment Processor Closed Our Account"

Unexpected account termination can happen with little notice.

For businesses relying entirely on online payments, this can immediately stop revenue generation.

"Our Chargebacks Keep Increasing"

Chargebacks don't just result in financial losses.

High dispute ratios can lead to reserve increases, higher processing fees, or complete account closure if left unmanaged.

"No Provider Understands Our Industry"

One of the most frustrating experiences for high-risk merchants is being treated as a fraud risk simply because of their business category.

Working with providers that specialize in high-risk industries significantly improves the approval experience.

How to Choose the Right Merchant Account Provider

Before signing with any payment provider, ask these questions:

Do they specialize in high-risk merchant accounts?

Can they support international payment processing?

Do they offer multi-currency payment acceptance?

What is their average approval rate?

How are rolling reserves calculated?

What fraud prevention tools are included?

How do they help reduce chargebacks?

Can they support recurring billing?

Will the solution scale as your business grows?

Do they provide dedicated account management?

Choosing the right provider today can save months of operational disruption in the future.

Why Businesses Trust BoxCharge

At BoxCharge, we understand that payment processing is more than simply accepting credit cards.

For high-risk businesses, it's about maintaining stable cash flow, minimizing payment disruptions, and supporting long-term growth.

Our payment specialists work with a global network of acquiring partners to help businesses secure reliable merchant accounts that traditional providers often decline.

Whether you're processing domestic transactions or expanding internationally, BoxCharge helps businesses access payment solutions tailored to their industry, transaction volume, and risk profile.

Our solutions include:

High-Risk Merchant Accounts

Offshore Merchant Accounts

High-Risk Payment Gateways

Multi-Currency Payment Processing

Payment Gateway Integration

Fraud Prevention Tools

Chargeback Management Solutions

Cross-Border Payments Processing

Recurring Billing Support

Instead of forcing your business into a one-size-fits-all solution, we help you find a payment infrastructure built around your growth goals.

Ready to Find the Right Merchant Account?

If repeated application rejections, frozen funds, or unreliable payment processors are holding your business back, it's time to explore a payment solution built specifically for high-risk merchants.

Contact BoxCharge today to discuss your business requirements with our payment specialists and discover a merchant account solution designed to support your growth, improve payment stability, and help you accept payments confidently across global markets.